by Jennifer Kohlhepp | CM Magazine Featured

Removing the 16-Digit Card Number and Beyond

By Ahmet Alptekin and Bora Göknar

There were several news outlets reporting in February on Mastercard’s plan to remove the 16-digit card number from physical debit and credit cards.

One news article informed that the company spoke to an Australian bank and a rollout plan was agreed upon. 1 According to the plan, the card numbers would not exist on credit and debit cards issued by 2030.

We would like to share our analysis of the initiative and present alternative strategies that may be equally effective while highlighting key considerations that retail banking heads and CEOs of issuer banks should take into account.

Let’s begin with how the structure of shared fees in credit card transactions has evolved, because understanding this evolution reveals the shifting center of power structure in the card payments ecosystem.

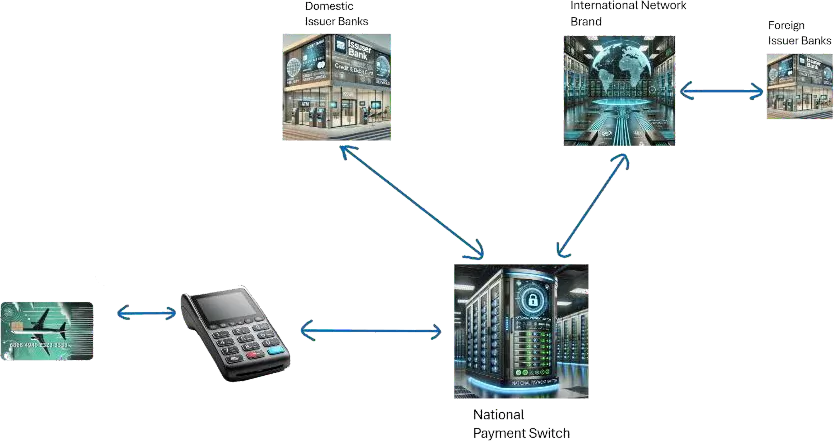

The Original Fee Model (Brand Networks at the Center)

In the early model, whenever a credit card issued by a domestic bank was used, the transaction would be routed through the acquiring bank and then to the card brand’s network. The brand network would relay the authorization request to the issuing bank, already a member of the brand’s ecosystem, and return an approval or decline message. The entire process, even for purely domestic transactions, went through the brand networks, resulting in fees paid to them by both issuers and acquirers.

Rise of National Switches Decentralizing the Network Brands’ Role

As domestic payment infrastructure matured, national switches emerged. For transactions where both the issuer and the merchant were domestic, these switches took over the routing, clearing and settlement tasks. This resulted in reducing the cost of domestic credit card transactions. Foreign issued cards were still routed through the global brand networks, but domestic transactions increasingly bypassed them. This significantly reduced the brand networks’ share of transaction fees, especially in markets where most transactions were domestic.

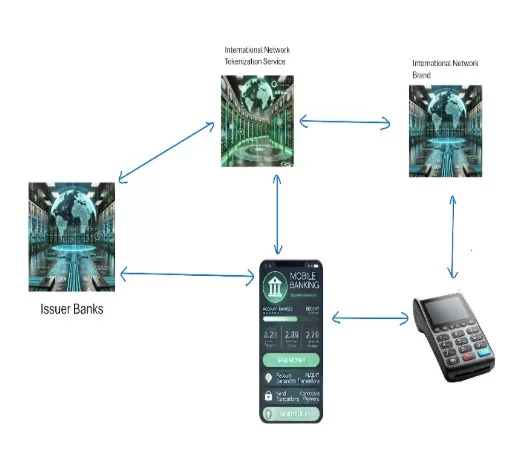

Reclaiming Fees with Online and Mobile

Then came the online transactions and mobile. The growth of e-commerce and mobile payments brought new security challenges. Brand networks responded with innovations like 3D Secure (3DS) for online transactions and tokenization for mobile. These technologies not only improved security but also re-established the networks at the core of digital transaction flows. Whether the card was domestic or international, these digital transactions now had to go through the brand networks reclaiming the fees that national switches had previously disrupted.

Removing the 16 digits from the physical card, if it will result in removing the physical card from the payment flow and if it is replaced by a virtual card, will result in all card payment transactions to go through the network brand systems. Thus, not only for mobile but for all card transactions, not only for international but also for domestic transactions including in-store payments, the issuer and the acquirer will pay transaction fees to the brand networks. This effectively resets the fee structure.

Tokenization is surely a nice technology that will reduce online fraud, however, at the expense of the issuer and acquirer banks.

We recommend looking at posts published last year focusing on the main benefits of the physical payment cards for the issuers. Here are five strategic advantages of physical payment cards that are often overlooked. 2

An additional and new argument that is relevant nowadays, due to the ongoing deglobalization trends we see, should be added to the list. Imagine what kind of additional burden would be inflicted on issuer banks if there is one more new mobile OS platform that they have to support. Today, they have to support their mobile banking apps for at least two platforms—Android and iOS. With the recent announcement of Huawei that they will start using their own mobile OS platform called HarmonyOS NEXT for their newer smartphone models, there is a real concern that surrounds the issuers in terms of their digital strategies, especially around digital payments. Is it possible that they will have to support a third mobile app to service their customers?

Imagine if issuer banks lose their exclusivity of the payment cards ownership advantage they have today, how would digital payments be reshaped. Chinese companies manufacture and ship more than 50% of the global smartphones. In a world where technology is weaponized extensively especially in the past decade, would other Chinese brands start supporting HarmonyOS NEXT? In that case, would banks be forced to support a third or a fourth smartphone platform to access all their customer base? These are all questions our industry needs to think about now.

Without a doubt, the payment industry is experiencing a profound evolution, impacting not only card issuance but also significantly transforming the acquiring and payment acceptance sectors. This rapid change is largely fueled by the increased adoption of software Point-of-Sale (SoftPOS) technologies, commonly known as “Tap to Phone” or “Tap on Phone” solutions.

Thanks to recent PCI regulatory updates, these solutions are now widely available and in use across the market.

With an estimated 180 million merchants worldwide still accepting only cash payments, this technological advancement is crucial for extending secure card transactions to both online and physical environments for these businesses. Furthermore, the global payment acceptance landscape is increasingly embracing alternative payment technologies such as digital wallets, QR codes and biometrics, which are also driving significant shifts in the ecosystem. Payment schemes are actively supporting this evolution, adapting their technologies and regulations to meet evolving customer demands. They are also instrumental in developing “Tap to More” technologies, which allow cardholders to use their personal devices for payment acceptance. This signifies a move away from traditional physical POS terminals, enabling cardholders to conduct card-present contactless transactions directly via their own devices; a development poised to significantly impact cardholder behaviors.

One implementation of Tap To More technology is “Tap to Own Device,” a technology that has the potential to bring the same level of security without disturbing the transaction fee structure the issuers and acquirers have been accustomed to since the beginning of card payments. This technology is an innovative answer to secure online transactions; now is the perfect time to seriously think about the global expansion strategies of the “Tap to Own Device” solution. You can read about or watch the detail of the technology.3,4 To give further detail, the “Tap on Own Device” solution allows for making an online payment transaction with your own physical payment card simply by tapping your own card on your own smartphone device to make the payment for an online transaction.

“Tap to Own Device” technology is set to transform payment interactions through two key applications. The first involves in-app transactions: while using a merchant’s mobile application, cardholders gain the flexibility to not only use a stored card but also to physically tap their payment card to their own device to complete the purchase. Crucially, this maintains the security and benefits of a card-present transaction by utilizing the cardholder’s personal mobile device.

The second exciting use case emerges in online checkout flows. Here, a website can generate a QR code that the cardholder scans with their device. This action launches an application on their device, which then enables them to complete the payment by simply tapping their card to their own phone. This means whether buying online or within a merchant’s app, “Tap to Own Device” empowers cardholders to execute secure, card-present transactions directly from their personal mobile technology, fundamentally altering payment behaviors.

Banks and the smartcard payment industry have the opportunity to prove that chip cards deliver undeniable value to all stakeholders. By boldly driving innovation in card payments, banks can position physical cards at the heart of their value propositions, leveraging mobile channels to enhance; not replace; their digital payment strategies. The future of payments should not be about choosing between physical cards and mobile but about harnessing their combined strength to shape a seamless, secure and strong payment ecosystem.

Resources

1 Your next credit card might not have any numbers. Here’s why

About the Authors: Bora Göknar is the senior vice president of sales & partnerships at Yazara, with more than a decade of experience in the financial technology sector. Based in Germany, he leads business development, account management and the formation of strategic partnerships on a global scale. He oversees a sales team composed of customer success managers and business development managers. Bora possesses deep expertise in digital and mobile payment systems, omni-channel banking products, wallets and NFC payments. In recent years, his focus has been on SoftPOS (Tap on Phone) solutions, fostering strong relationships with customers, partners and global payment schemes. His extensive knowledge of the financial landscape and innovative payment technologies positions him as a trusted industry leader. Outside of work, Bora is a certified cook who loves experimenting in the kitchen, and a keen cyclist who rarely misses a daily ride—unless it rains.

With more than 20 years of experience in the digital payments ecosystem, Ahmet Alptekin brings deep expertise in smart card technologies and secure payment systems. His career spans strategic business development, solution sales and product marketing across regions including the Middle East, Africa and Southern and Eastern Europe. He has successfully led market expansion initiatives, delivered innovative projects and contributed to global industry efforts. With a background in engineering and business administration, Ahmet blends technical and commercial insights to help drive innovation in the digital transformation age. Outside of his professional work, he enjoys developing mobile apps, some of which support educational institutions. Based in Dubai, Ahmet is a husband as well as a father to his daughter and son. He is also an amateur author with a passion for memoirs and a collector of keychains.